Project Management, Finance Management, Resource Management

The Straight-Line Method of Depreciation

In the realm of accounting and asset management, depreciation is a concept that plays a pivotal role, particularly in industries like construction. Among the various methods used to calculate depreciation, the Straight-Line Method stands out as one of the simplest yet most widely employed. In this article, we will explore what the Straight-Line Method of depreciation is, how it works, and why it matters in the context of construction and other industries.

Understanding Depreciation

Before delving into the specifics of the Straight-Line Method, let's grasp the essence of depreciation itself. Depreciation is the process of allocating the cost of a tangible asset over its useful life. In simpler terms, it's a way of accounting for the wear and tear, obsolescence, and aging that assets undergo as they are used in a business.

Depreciation serves two essential purposes:

- Financial Reporting: Depreciation expenses are recorded on a company's income statement, reflecting the reduction in the asset's value over time. This is crucial for accurate financial reporting and tax compliance.

- Asset Replacement Planning: Depreciation helps businesses plan for the eventual replacement or upgrade of assets. By understanding how much an asset has depreciated, a company can budget for its replacement when the time comes.

The Straight-Line Method Demystified

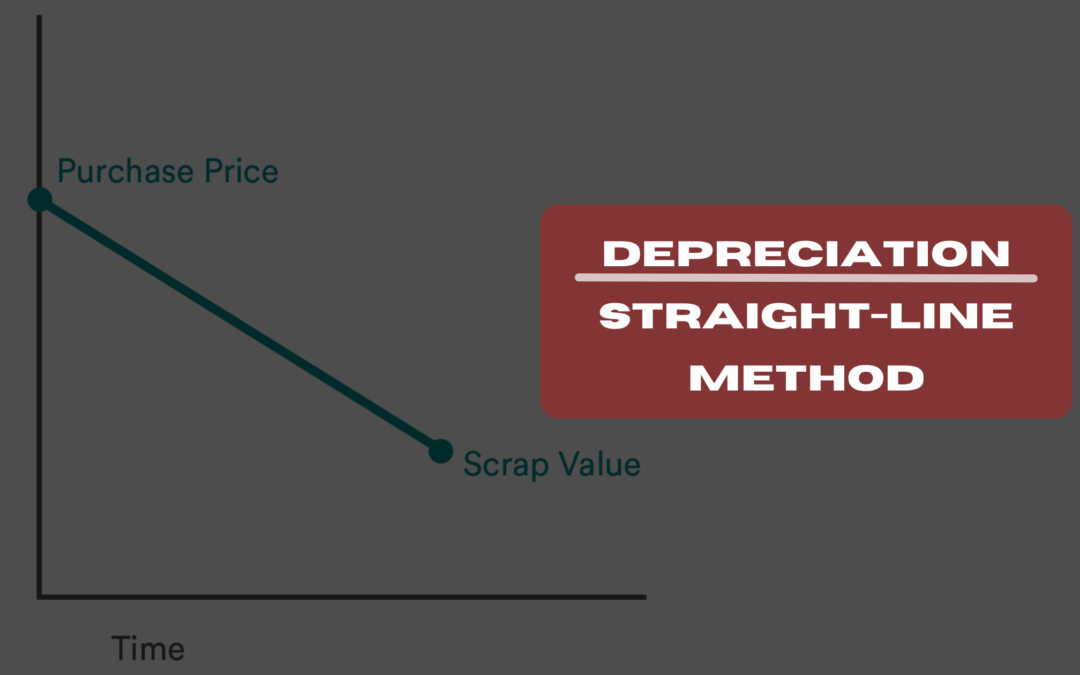

The Straight-Line Method is a depreciation technique that evenly spreads the cost of an asset over its estimated useful life. Here's how it works:

Formula:

[Depreciation = \frac{Cost of Asset - Salvage Value}{Useful Life}]

- Cost of Asset: The initial cost of the asset, including any expenses related to its acquisition, such as delivery and installation.

- Salvage Value: The estimated residual value of the asset at the end of its useful life. This is the amount the asset is expected to be worth when it's no longer in use.

- Useful Life: The anticipated number of years or units of production during which the asset will be used by the business.

An Example in Practice

Let's consider a practical example to illustrate the Straight-Line Method.

Imagine a construction company in India purchases a heavy-duty crane for ₹10,00,000. They estimate that the crane will have a useful life of 10 years and expect to sell it as scrap for ₹1,00,000 when it reaches the end of its operational life.

Using the Straight-Line Method, the annual depreciation for the crane can be calculated as follows:

[Depreciation = \frac{Cost of Asset - Salvage Value}{Useful Life}]

[Depreciation = \frac{₹10,00,000 - ₹1,00,000}{10}]

[Depreciation = \frac{₹9,00,000}{10}]

[Depreciation = ₹90,000 per year]

So, according to the Straight-Line Method, the company will record ₹90,000 as depreciation expense on their financial statements for the crane each year.

Why the Straight-Line Method Matters

The Straight-Line Method is favored by businesses for several reasons:

- Simplicity: It's easy to understand and calculate, making it accessible even for small businesses and individuals.

- Consistency: The depreciation expense remains the same each year, simplifying financial planning and budgeting.

- Equitable: It evenly spreads the cost of the asset's use over its life, making it a fair method for allocating expenses.

However, it's important to note that while the Straight-Line Method is straightforward, it may not always reflect the actual pattern of an asset's depreciation. Some assets may lose value more rapidly in the earlier years, while others may have a more uneven pattern. In such cases, alternative depreciation methods like the Declining Balance Method may be more appropriate.

In conclusion, the Straight-Line Method of depreciation is a fundamental accounting approach used to allocate the cost of an asset evenly over its useful life. It provides a clear and consistent way to account for an asset's decreasing value and is widely used in construction equipment management and financial reporting. Understanding depreciation and its various methods is essential for businesses to make informed financial decisions and plan for the future.

Resource Management, Finance Management, Project Management

Factors and Methods of Depreciation in Construction Equipment

In the world of construction, equipment is the unsung hero, powering the creation of infrastructure, buildings, and landmarks. However, as these mighty machines perform their duties day in and day out, they undergo a natural process known as depreciation. Depreciation is a crucial concept in construction equipment management and financial accounting, affecting a company's balance sheet and decision-making processes. In this article, we will delve into the intricacies of depreciation, exploring what it is, why it happens, and the different methods used to calculate it.

Defining Depreciation

Depreciation refers to the gradual decrease in the value of an asset over its useful life. In the context of construction equipment, it represents the diminishing worth of machinery as it experiences wear and tear, obsolescence, and the passage of time. Depreciation is an accounting method used to accurately reflect an asset's declining value on a company's financial statements.

The Factors Behind Equipment Depreciation

Several factors contribute to the depreciation of construction equipment. Understanding these factors is essential for effective equipment management:

1. Physical Wear and Tear

Why it matters: Construction equipment operates in demanding environments, often exposed to heavy loads, vibrations, and harsh weather conditions. The physical wear and tear resulting from these conditions lead to a gradual deterioration of equipment components, affecting its performance and value.

Takeaway: Regular maintenance and inspections are crucial to mitigate the effects of wear and tear and extend equipment lifespan.

2. Technological Obsolescence

Why it matters: The construction industry continually evolves with advancements in technology. Newer equipment models often come with improved efficiency, safety features, and environmental compliance. As technology progresses, older equipment may become outdated and less competitive.

Takeaway: Staying updated with technological advancements and periodically assessing equipment for obsolescence can help in managing depreciation.

3. Market Demand and Supply

Why it matters: The resale value of used construction equipment is influenced by market dynamics. Oversupply of specific equipment types or reduced demand can lead to lower prices in the resale market, contributing to depreciation.

Takeaway: Keeping an eye on market trends and demand for specific equipment can aid in decision-making regarding equipment acquisition and disposal.

4. Maintenance Costs

Why it matters: Neglecting maintenance or failing to address issues promptly can result in higher repair costs. Inadequate maintenance practices can lead to more extensive damage, accelerating depreciation.

Takeaway: Implementing a proactive maintenance schedule can help control costs and minimize the impact of depreciation.

5. Usage Intensity

Why it matters: Equipment subjected to heavy and continuous use is more likely to experience faster depreciation. High usage leads to increased wear on critical components, shortening their lifespan.

Takeaway: Monitoring equipment usage patterns and ensuring that equipment is allocated efficiently can help extend its lifespan.

6. Equipment Age

Why it matters: Older equipment tends to depreciate faster than newer models. The wear and tear accumulated over the years, combined with the lack of modern features, contribute to reduced value.

Takeaway: Assessing equipment age and planning for timely replacements or upgrades is essential for managing depreciation.

Different Methods for Calculating Depreciation

Several methods are used to calculate depreciation, each with its own advantages and implications. Here are some common depreciation calculation methods:

1. Straight-Line Depreciation

How it works: This method spreads the depreciation expense evenly over the asset's useful life. It is simple to calculate and provides a steady and predictable expense pattern.

Use case: Straight-line depreciation is suitable for assets with a relatively uniform rate of wear and tear.

2. Declining Balance Depreciation

How it works: Declining balance depreciation applies a higher depreciation expense in the early years of an asset's life. It reflects the higher maintenance and repair costs typically associated with older equipment.

Use case: This method is suitable when equipment tends to require more maintenance as it ages.

3. Units of Production Depreciation

How it works: Depreciation is calculated based on the actual usage or production output of the equipment. The more the equipment is used, the higher the depreciation expense.

Use case: Units of production depreciation is ideal for equipment where usage varies significantly.

4. Sum-of-the-Years-Digits Depreciation

How it works: This method accelerates depreciation by assigning higher expenses in the earlier years of an asset's life. It provides a middle ground between straight-line and declining balance depreciation.

Use case: Sum-of-the-years-digits depreciation suits assets that experience moderate wear and tear.

5. Double Declining Balance Depreciation

How it works: A variation of declining balance depreciation, this method doubles the rate of depreciation in comparison to the declining balance method.

Use case: It is used for assets that experience rapid wear and tear, especially in their early years.

6. MACRS (Modified Accelerated Cost Recovery System)

How it works: MACRS is a tax-related depreciation method used in the United States. It assigns specific depreciation rates based on asset types and their useful lives.

Use case: MACRS is primarily used for tax purposes and is specific to U.S. tax regulations.

In Conclusion

Depreciation is an inherent aspect of owning and managing construction equipment. It accounts for the natural wear and tear, technological advancements, and market fluctuations that equipment undergoes over time. By understanding the factors contributing to depreciation and selecting appropriate depreciation calculation methods, construction professionals can make informed decisions about equipment acquisition, maintenance, and replacement.

Effective depreciation management not only ensures accurate financial reporting but also contributes to efficient equipment utilization and cost control in the construction industry. In this ever-evolving field, staying informed and proactive is the key to maximizing the value and longevity of construction equipment.

"The best way to predict your future is to create it." - Abraham Lincoln

Investing in proper equipment management and depreciation strategies is how construction professionals shape a successful future in this dynamic industry.

Finance Management

What is GAAP

GAAP (Generally Accepted Accounting Principles) is a collection of commonly followed accounting rules and standards for financial reporting. The acronym is pronounced gap.

What Are the Principles of Accounting?

The best way to understand the GAAP requirements is to look at the ten principles of accounting.

1. ECONOMIC ENTITY PRINCIPLE

The business is considered a separate entity, so the activities of a business must be kept separate from the financial activities of its business owners.

2. MONETARY UNIT PRINCIPLE

The monetary unit assumption means that only transactions in U.S. dollar amounts can be included in accounting records. It’s important to note that accountants ignore the effects of inflation on the recorded dollar amounts.

3. TIME PERIOD PRINCIPLE

The business activities may be reported in short, distinct time intervals which may be weeks, months, quarters, a calendar year, or a fiscal year. The time interval has to be identified in the headings of the financial statements such as the income statement, statement of cash flow, and stockholders’ equity statement.

4. COST PRINCIPLE

The cost principle mentions the historical cost of an item. This refers to cash or cash equivalent that was paid to purchase an item in the past. This asset amount is adjusted for inflation. The historical cost is reported on the financial statements.

5. FULL DISCLOSURE PRINCIPLE

All information that is relative to the business and is important to a lender or investor must be disclosed in the content of the financial statements or in the notes to the statements. This is the reason that numerous footnotes are attached to financial statements

6. GOING CONCERN PRINCIPLE

This accounting principle refers to the intent of a business to carry on its operations and commitments into the foreseeable future and not to liquidate the business.

7. MATCHING PRINCIPLE

The matching principle requires that businesses use the accrual basis of accounting and match business income to business expenses in a given time period.

For example, the commissions for sales should be recorded in the same accounting period that sales income was made (and not when they were paid).

8. REVENUE RECOGNITION PRINCIPLE

Under the accrual basis of accounting, the revenues must be reported on the income statement in the period in which it is earned. This means that as soon as a product is sold, or the service has been performed, the revenues are recognized. This is regardless of whether the money is received or not.

9. MATERIALITY PRINCIPLE

The materiality principle refers to the misstatement in accounting records when the amount is insignificant or immaterial. Because of the materiality principle, financial statements usually show amounts rounded to the nearest dollar.

10. CONSERVATISM PRINCIPLE

If accountants are unsure about how to report an item, the conservatism principle calls for potential expenses and liabilities to be recognized immediately. It directs the accountant to anticipate the losses and choose the alternative that will result in less net income and/or less asset amount.

What Are the 10 Principles of GAAP?

There are ten principles that can help you understand the mission of the GAAP standards and rules.

1. PRINCIPLE OF REGULARITY

The principle states that the accountant has complied to the GAAP rules and regulations.

2. PRINCIPLE OF CONSISTENCY

The accountants should enter all items in exactly the same way that it has been fixed. By applying similar standards in the reporting process, accountants can avoid errors or discrepancies.

If the standards are changed or updates, the accountants are expected to fully disclose and explain the reasons behind the changes.

3. PRINCIPLE OF SINCERITY

As per this principle, the accountant should provide the correct depiction of the financial situation of a business.

4. PRINCIPLE OF PERMANENCE OF METHOD

The focus of this principle is that there should be a consistency in the procedures used in financial reporting.

5. PRINCIPLE OF NON-COMPENSATION

The full details of the financial information should be disclosed including negatives and positives. This should be done without the expectation of debt compensation by an asset or revenue by an expense.

6. PRINCIPLE OF PRUDENCE

The financial data representation should be done “as it is” and not based on any speculation.

7. PRINCIPLE OF CONTINUITY

The principle assumes that the business will continue its operations in the future.

8. PRINCIPLE OF PERIODICITY

The accounting entries are distributed across the suitable time periods.

9. PRINCIPLE OF FULL DISCLOSURE

While creating the financial reports, the accountants must strive for full disclosure.

10. PRINCIPLE OF UTMOST GOOD FAITH

This principle states presupposes that the parties remain honest in transactions.