The Straight-Line Method of Depreciation

In the realm of accounting and asset management, depreciation is a concept that plays a pivotal role, particularly in industries like construction. Among the various methods used to calculate depreciation, the Straight-Line Method stands out as one of the simplest yet most widely employed. In this article, we will explore what the Straight-Line Method of depreciation is, how it works, and why it matters in the context of construction and other industries.

Table of Contents

Understanding Depreciation

Before delving into the specifics of the Straight-Line Method, let's grasp the essence of depreciation itself. Depreciation is the process of allocating the cost of a tangible asset over its useful life. In simpler terms, it's a way of accounting for the wear and tear, obsolescence, and aging that assets undergo as they are used in a business.

Depreciation serves two essential purposes:

- Financial Reporting: Depreciation expenses are recorded on a company's income statement, reflecting the reduction in the asset's value over time. This is crucial for accurate financial reporting and tax compliance.

- Asset Replacement Planning: Depreciation helps businesses plan for the eventual replacement or upgrade of assets. By understanding how much an asset has depreciated, a company can budget for its replacement when the time comes.

The Straight-Line Method Demystified

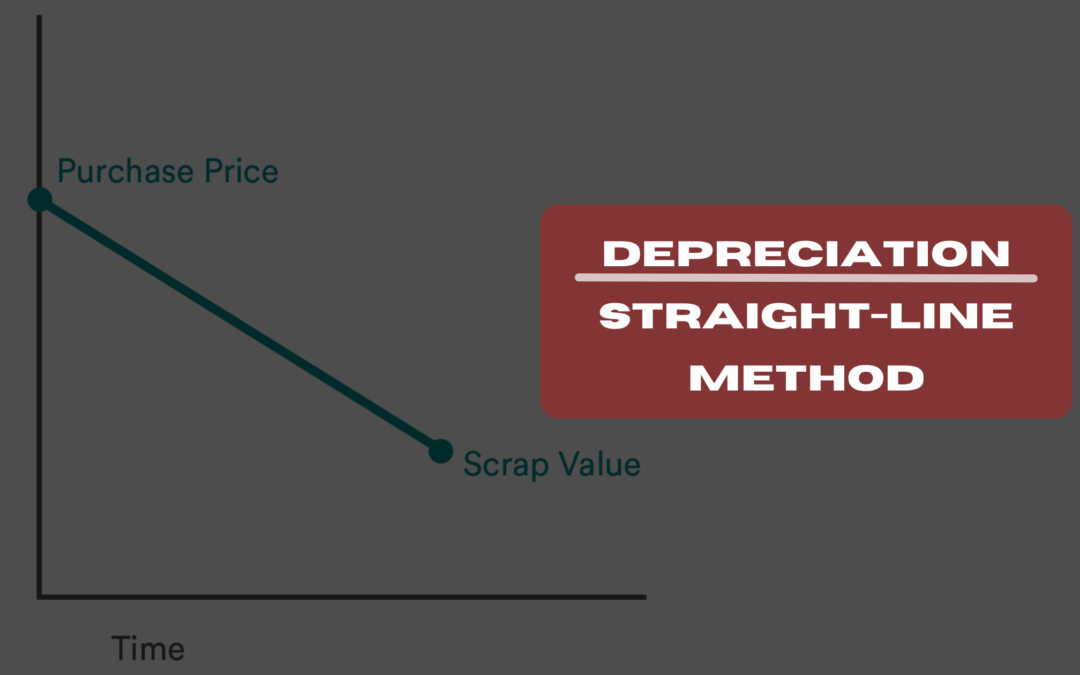

The Straight-Line Method is a depreciation technique that evenly spreads the cost of an asset over its estimated useful life. Here's how it works:

Formula:

[Depreciation = \frac{Cost of Asset - Salvage Value}{Useful Life}]

- Cost of Asset: The initial cost of the asset, including any expenses related to its acquisition, such as delivery and installation.

- Salvage Value: The estimated residual value of the asset at the end of its useful life. This is the amount the asset is expected to be worth when it's no longer in use.

- Useful Life: The anticipated number of years or units of production during which the asset will be used by the business.

An Example in Practice

Let's consider a practical example to illustrate the Straight-Line Method.

Imagine a construction company in India purchases a heavy-duty crane for ₹10,00,000. They estimate that the crane will have a useful life of 10 years and expect to sell it as scrap for ₹1,00,000 when it reaches the end of its operational life.

Using the Straight-Line Method, the annual depreciation for the crane can be calculated as follows:

[Depreciation = \frac{Cost of Asset - Salvage Value}{Useful Life}]

[Depreciation = \frac{₹10,00,000 - ₹1,00,000}{10}]

[Depreciation = \frac{₹9,00,000}{10}]

[Depreciation = ₹90,000 per year]

So, according to the Straight-Line Method, the company will record ₹90,000 as depreciation expense on their financial statements for the crane each year.

Why the Straight-Line Method Matters

The Straight-Line Method is favored by businesses for several reasons:

- Simplicity: It's easy to understand and calculate, making it accessible even for small businesses and individuals.

- Consistency: The depreciation expense remains the same each year, simplifying financial planning and budgeting.

- Equitable: It evenly spreads the cost of the asset's use over its life, making it a fair method for allocating expenses.

However, it's important to note that while the Straight-Line Method is straightforward, it may not always reflect the actual pattern of an asset's depreciation. Some assets may lose value more rapidly in the earlier years, while others may have a more uneven pattern. In such cases, alternative depreciation methods like the Declining Balance Method may be more appropriate.

In conclusion, the Straight-Line Method of depreciation is a fundamental accounting approach used to allocate the cost of an asset evenly over its useful life. It provides a clear and consistent way to account for an asset's decreasing value and is widely used in construction equipment management and financial reporting. Understanding depreciation and its various methods is essential for businesses to make informed financial decisions and plan for the future.